At the same time, however, these numbers don’t lie. With our demographics and our debts, we’re on a collision course with the future. The good news: Although time is growing short, we still have the capacity to create positive outcomes.

Even though USA Inc. can print money and raise taxes, USA Inc. cannot sustain its financial imbalance indefinitely – especially as the Baby Boomer generation nears retirement age. Net debt levels are approaching warning levels, and some polls suggest that Americans consider reducing debt a national priority. Change is legally possible. Unlike underfunded pension liabilities that can

bankrupt companies, USA Inc.’s underfunded liabilities are not legal contracts.

Congress has the authority to change the level and conditions for Social Security and Medicare benefits; the federal government, together with the states, can also alter eligibility and benefit levels for Medicaid.

Options for entitlement reform, operating efficiency, and stronger long-term GDP growth.

As analysts, not public policy experts, we can offer mathematical illustrations as a framework for discussion (not necessarily as actual solutions).

We also present policy options from third-party organizations such as the CBO.

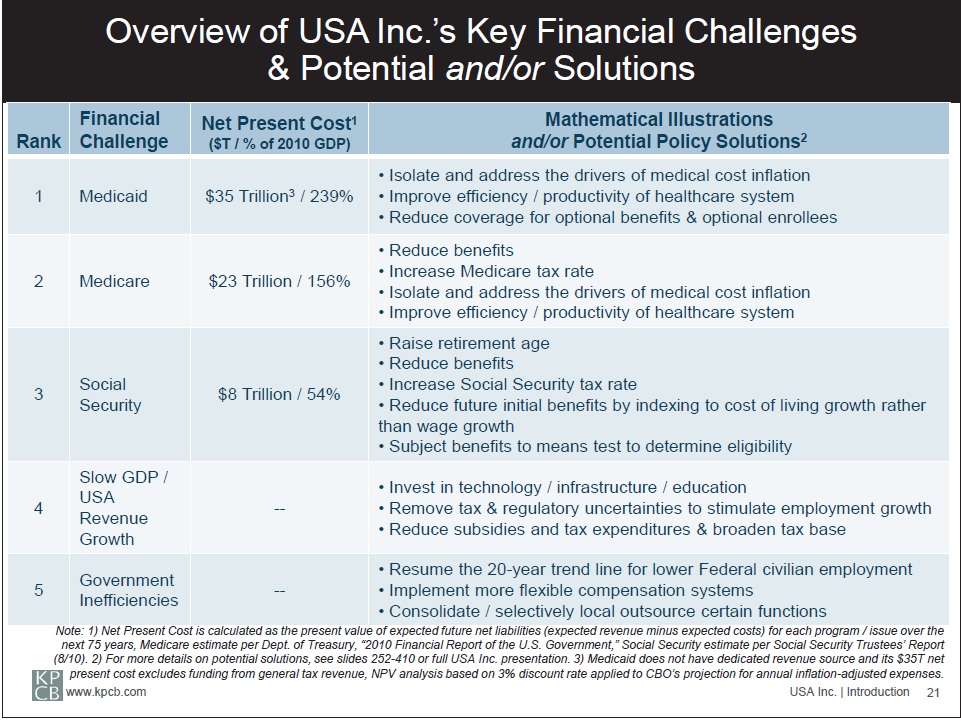

Reforming entitlement programs – Social Security.

Reforming entitlement programs – Medicare and Medicaid.

Improving operating efficiency.

Improving long-term GDP growth – productivity and employment.

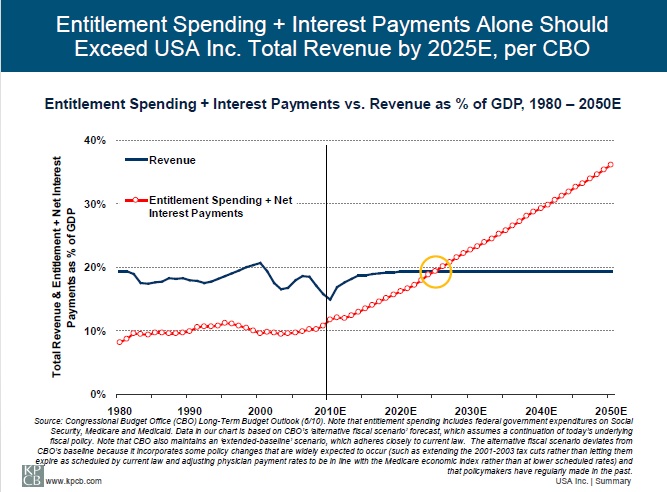

How Much Would Real GDP Need to Grow to Drive USA Inc. to Break-Even Without Policy changes? 6-7% in F2012E-F2014E &4-5% in F2015- F2020EWell Above 40-Year Average of 3%

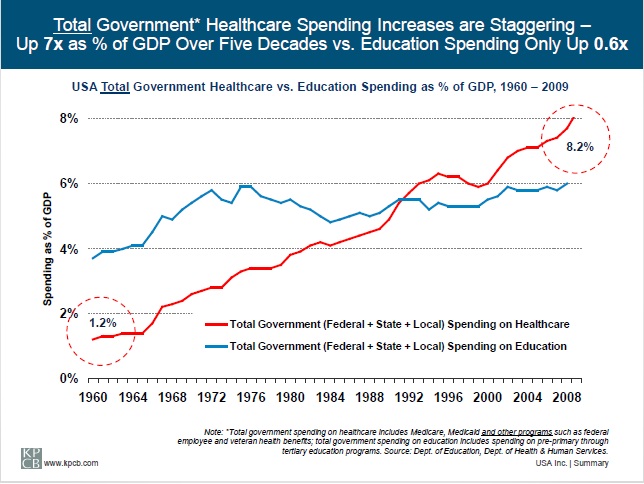

Since the 1960s, as more resources have gone to entitlements and interest payments, USA Inc. has scaled back its investment in technology R&D and infrastructure as percentages of GDP. Competitors are making these investments.

India plans to double infrastructure spending as a percent of GDP by 2013, and its tertiary (college) educated population will double over the next ten years, according to Morgan Stanley analysts, enabling its GDP growth to accelerate to 9-10% annually by 2015 (China’s annual GDP growth is forecast to remain near 8% by 2015). USA Inc. can’t match India’s demographic advantage, but technology can help.

For employment gains, USA Inc. should minimize tax and regulatory uncertainties and encourage businesses to add workers. While hiring and R&D-related tax credits may add to near-term deficits, over time, they should drive job and GDP growth. Immigration reform could also help: A Federal Reserve study in 2010 shows that immigration does not take jobs from U.S.-born workers but boosts productivity and income per worker.

Changing tax policies.

These issues are undoubtedly complex, and difficult decisions must be made. But inaction may be the greatest risk of all. The time to act is now, and our first responsibility as investors in USA Inc. is to understand the task at hand.

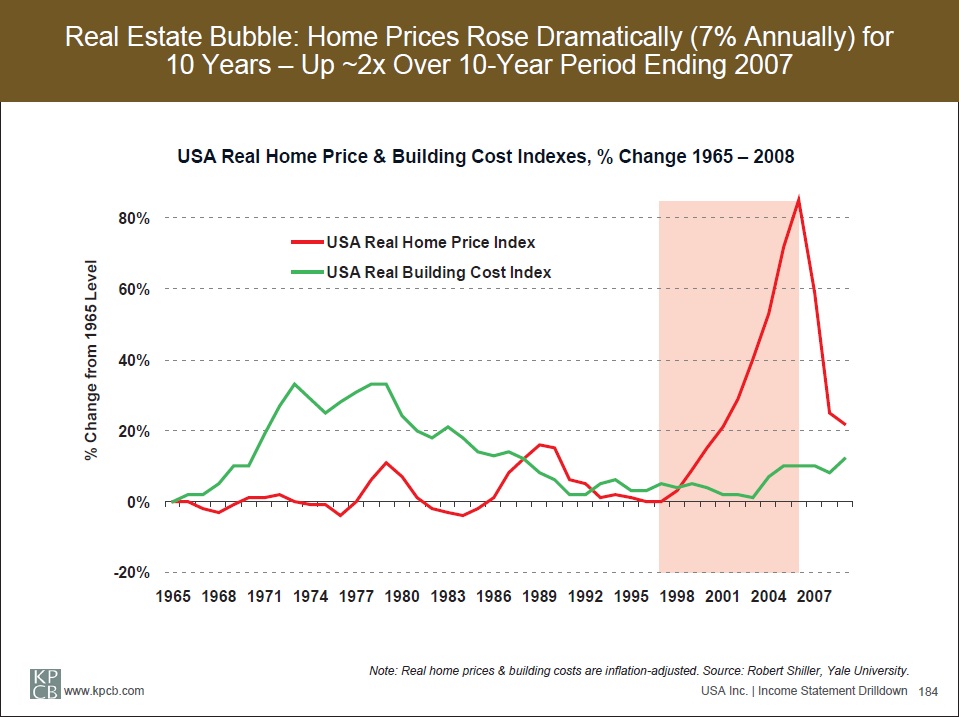

America’s Resources Allocated to Housing + Healthcare Nearly Doubled as a Percent of GDP Since 1965, While Household and Government Savings Fell Dramatically

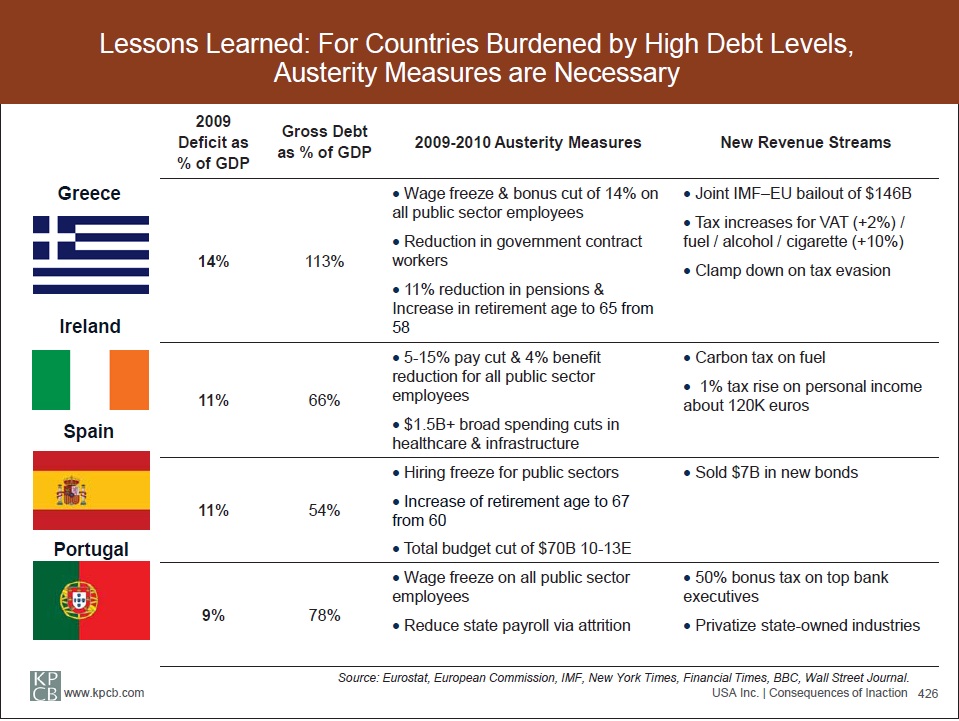

Common principles for overcoming this kind of burden include the following:

1) Acknowledge the problem – some 80% of Americans believe ‘dealing with our growing budget deficit and national debt’ is a national priority, according to a Peter G. Peterson Foundation survey in 11/09;

2) Examine past errors – People need clear descriptions and analysis to understand how the US arrived at its current financial condition – a ‘turnaround CEO’ would certainly initiate a ‘no holds barred’ analysis of the purpose, success and operating efficiency of all of USA Inc.’s spending;

3) Make amends for past errors – Most Americans today at least acknowledge the problems at personal levels and say they rarely or never spend more than what they can afford (63% according to a 2007 Pew Research study). The average American knows the importance of managing a budget. Perhaps more would be willing to sacrifice for the greater good with an understandable plan to serve the country’s long-term best interests;

4) Develop a new code of behavior – Policymakers, businesses (including investment firms), and citizens need to share responsibility for past failures and develop a plan for future successes.

Past generations of Americans have responded to major challenges with collective sacrifice and hard work. Will ours also rise to the occasion?

USA Inc. Concept

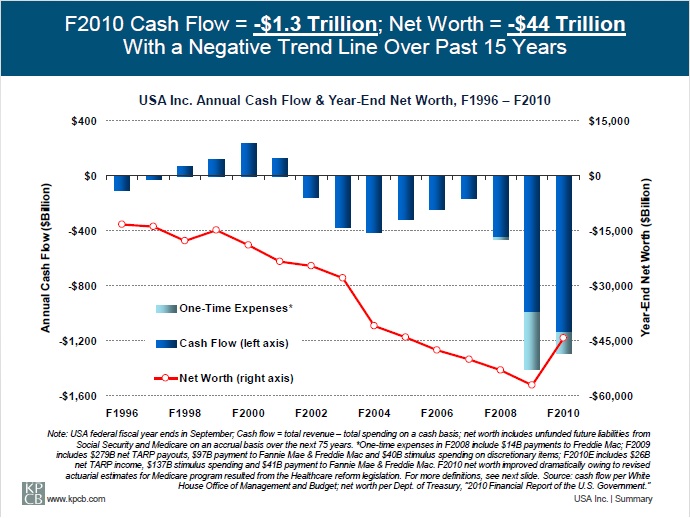

Healthy financials and compelling growth prospects are key to success for businesses (and countries). So if the US federal government – which we call USA Inc. – were a business, how would public shareholders view it?

How would long-term investors evaluate the federal government’s business model, strategic plans, and operating efficiency? How would analysts react to its earnings reports? Although some 45% of American households own shares in publicly traded companies and receive related quarterly financial statements, not many “stakeholders” look closely at Washington’s financials. Nearly two-thirds of all American households2 pay federal income taxes, but very few take the time to dig into the numbers of the entity that, on average, collects 13% of all Americans’ annual gross income (not counting another 15-30% for payroll and various state and local taxes).

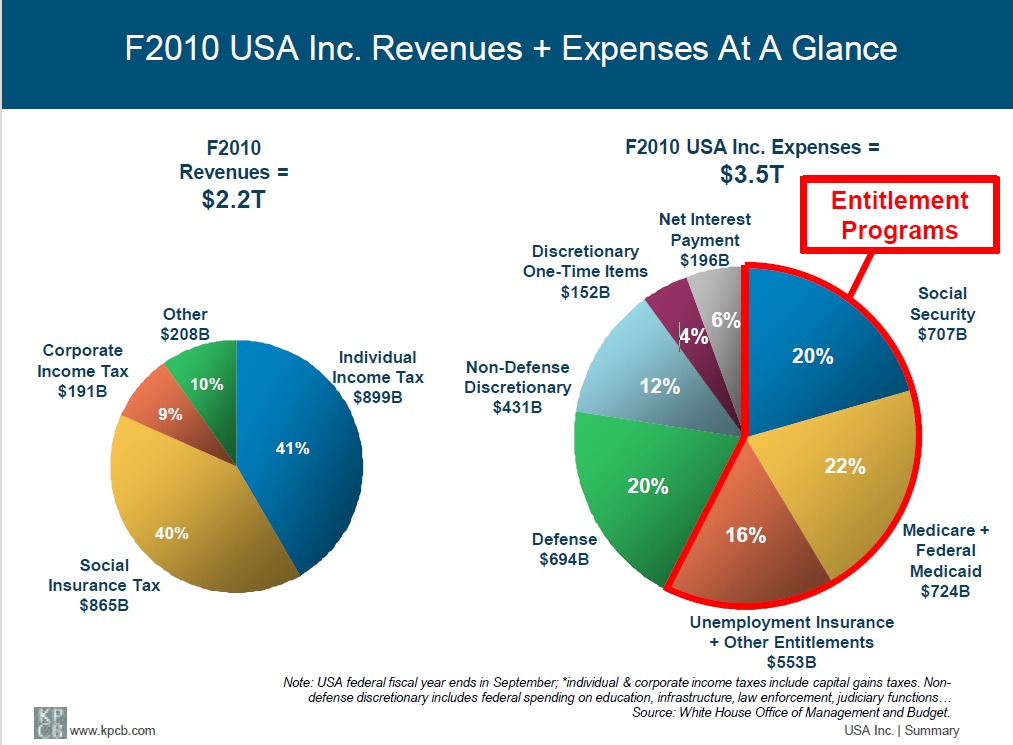

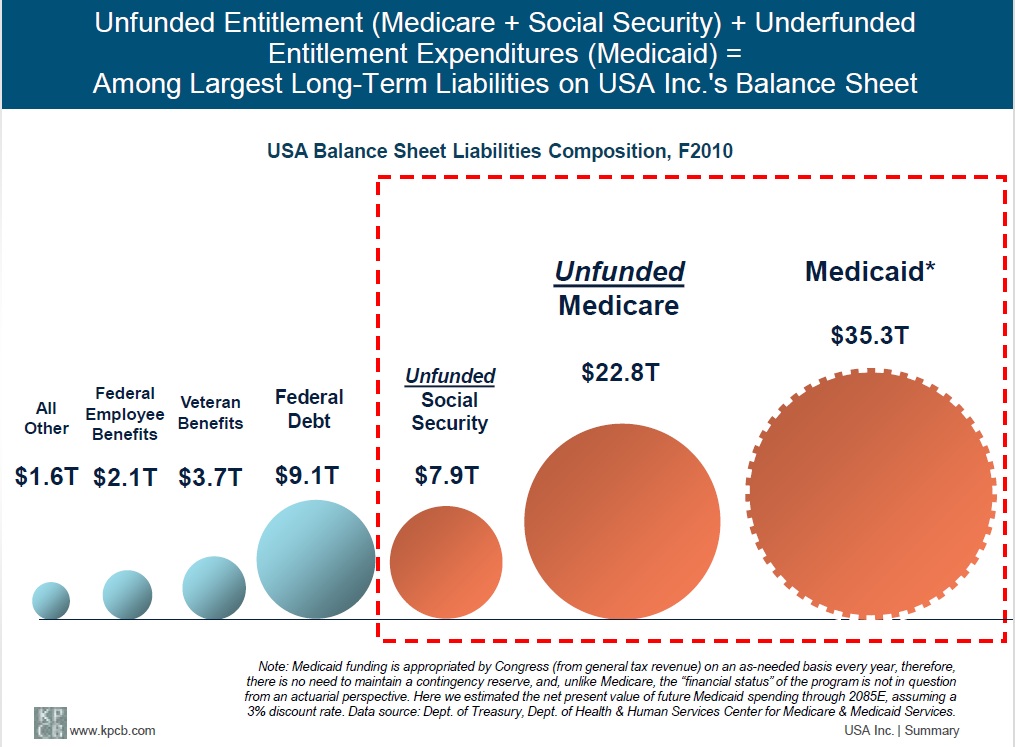

We drill down on USA Inc.’s past, present, and (in some cases) future financial dynamics and focus on the country’s income statement and balance sheet and related trends. We isolate and review key expense and revenue drivers. On the expense side, we examine the major entitlement programs (Medicare, Medicaid and Social Security) as well as defense and other major discretionary programs. On the revenue side, we focus on GDP growth (driven by labor productivity and employment in the long run) and tax policies.

We present basic numbers-driven scenarios for addressing USA Inc.'s financial challenges. In addition, we lay out the type of basic checklists that corporate turnaround experts might use as starting points when looking at some of USA Inc.’s business model challenges.